Bah humbug: The Christmas tax dilemma

Don’t want to pay tax on Christmas? Here are our top tips to avoid giving the Australian Tax Office a bonus this festive season.

1. Keep team gifts spontaneous

$300 is the minor benefit threshold for FBT so anything at or above this level will mean that your Christmas generosity will result in a gift to the ATO at a rate of 47%. To qualify as a minor benefit, gifts also have to be ad hoc - no monthly gym memberships or giving one person multiple gift vouchers amounting to $300 or more.

Gifts of cash from the business are treated as salary and wages – PAYG withholding is triggered and the amount is normally subject to the superannuation guarantee.

Aside from the tax issues, think about what will be of value to your team. The most appreciated gift is the one that means something to the individual. Giving a bottle of wine to someone who doesn’t drink, chocolates to a health fanatic, or time off to someone with excess leave, isn’t going to garner much in the way of goodwill. A sincere personal message will often have a greater impact than a generic gift.

2. The FBT Christmas party crunch

If you really want to avoid tax on your work Christmas party then host it in the office on a workday. This way, Fringe Benefits Tax (FBT) is unlikely to apply regardless of how much you spend per person. Also, taxi travel that starts or finishes at an employee’s place of work is exempt from FBT. So, if you have a few team members that need to be loaded into a taxi after overindulging in Christmas cheer, the ride home is exempt from FBT.

If your work Christmas party is out of the office, keep the cost of your celebrations below $300 per person if you want to avoid paying FBT. The downside is that the business cannot claim deductions or GST credits for the expenses if there is no FBT payable in relation to the party.

If the party is held somewhere other than your business premises, then the taxi travel is taken to be a separate benefit from the party itself and any Christmas gifts you have provided. In theory, this means that if the cost of each item per person is below $300 then the gift, party and taxi travel can potentially all be FBT-free. Just remember that the minor benefits exemption requires a number of factors to be considered, including the total value of associated benefits provided across the FBT year.

If entertainment is provided to employees and an FBT exemption applies, you will not be able to claim tax deductions or GST credits for the expenses.

If your business hosts slightly more extravagant parties and goes above the $300 per person minor benefit limit, you will pay FBT but you can also claim a tax deduction and GST credits for the cost of the event. Just bear in mind that deductions are only useful to offset against tax. If your business is paying no or limited amounts of tax, a tax deduction is not going to help offset the cost of the party.

3. Avoid client lunches and give a gift

The most effective way of sharing the Christmas joy with customers is not necessarily the most tax effective. If, for example, you take your client out or entertain them in any way, it’s not tax deductible and you can’t claim back the GST. There are specific rules designed to prevent deductions and GST credits from being claimed when the expenses relate to entertainment, regardless of whether there is an expectation of generating goodwill and increased business sales. Restaurants, a show, golf, and corporate race days all fall into the ‘entertainment’ category.

However, if you send your customer a gift, then the gift is tax deductible as long as there is an expectation that the business will benefit (assuming the gift does not amount to entertainment). Even better, why don’t you deliver the gift yourself for your best customers and personally wish them a Merry Christmas. It will have a much bigger impact even if they are not available and the receptionist tells them you delivered the gift.

From a marketing perspective, if your budget is tight, it’s better to focus on the customers you believe deliver the most value to your business rather than spending a small amount on every customer regardless of value. If you are going to invest in Christmas gifts, then make it something people remember and appropriate to your business.

You could also make a donation on behalf of your customers (where your business takes the tax deduction) or for your customers (where they receive the tax deduction).

4. Charities love cash

Charities love cash. They don’t have to spend any of their precious resources to receive it – unlike a lot of charity dinners, auctions, and promotional campaigns. And, from a tax perspective, it’s the safest way to ensure that you or your business can claim a deduction for the full amount of the donation.

There are a few rules to giving to charities that make the difference between whether you will or won’t receive a tax deduction.

The charity must be a deductible gift recipient (DGR). You can find the list of DGRs on the Australian Business Register (use the advanced search).

If you buy any form of merchandise for the ‘donation’ – biscuits, teddies, balls or you buy something at an auction – then it’s generally not deductible. Your donation needs to be a gift, not an exchange for something material. Buying a goat or funding a child’s education in the third world is generally ok because you are generally donating an amount equivalent to the cause rather than directly funding that thing.

The tax deduction for charitable giving over $2 goes to the person or entity who made the gift and whose name is on the receipt.

5. Christmas bonuses

If you are planning to provide your team with a cash bonus rather than a gift voucher or other item of property, then remember that this will be taxed in much the same way as salary and wages. A PAYG withholding obligation will be triggered and the ATO’s view is that the bonus will also be treated as ordinary time earnings (unless it relates specifically to overtime work) which means that it will be subject to the superannuation guarantee provisions.

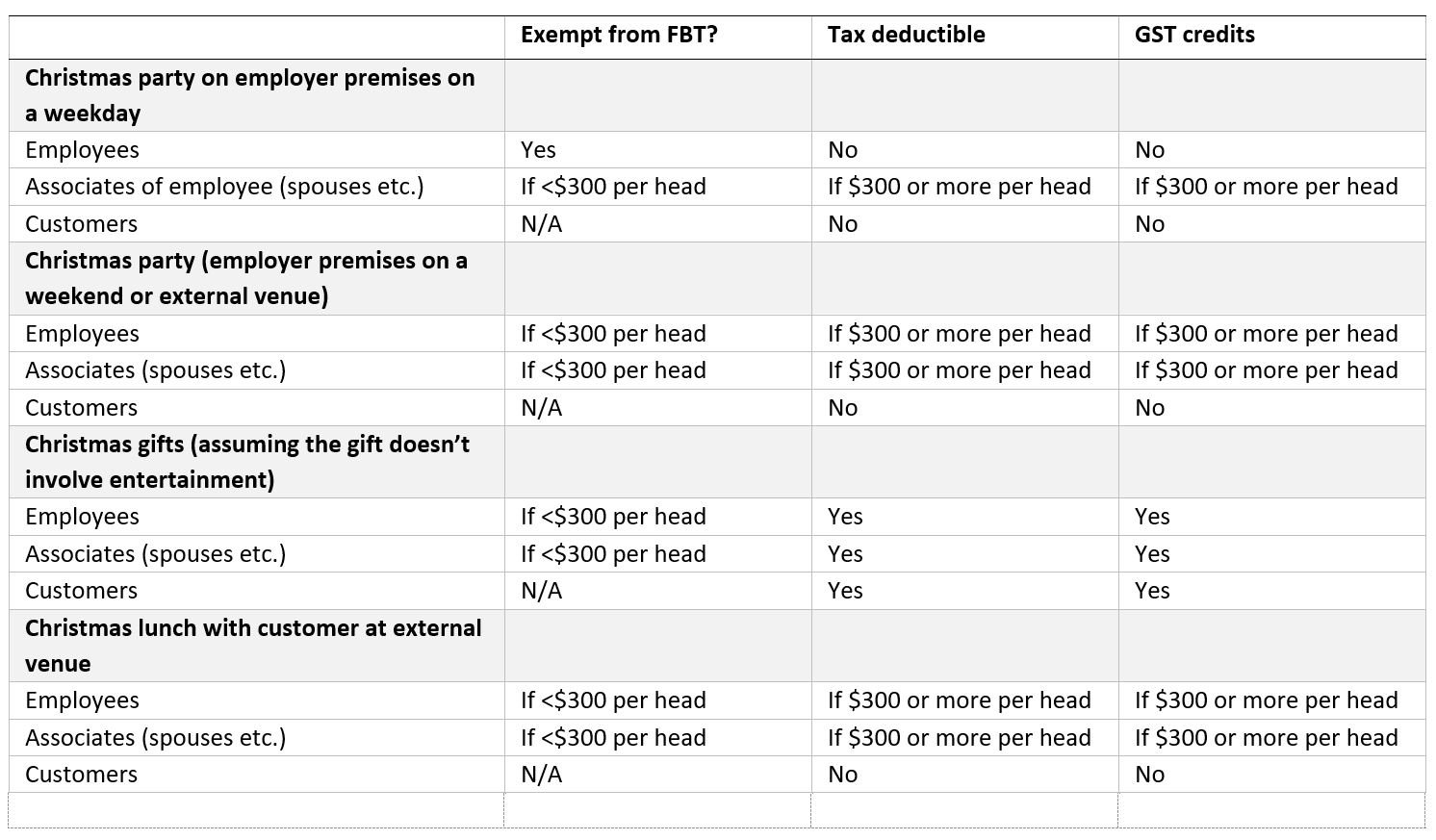

The Christmas tax quick guide

Here’s our quick guide to the tax impact of Christmas celebrations. The information is for GST registered businesses that are not using the 50-50 split method for meal entertainment.